Bottom line: FFIEC cybersecurity expectations are not just a compliance checklist. For community banks and financial institutions, they are a practical roadmap for proving that cyber risk is governed, measured, tested, and ready for real disruption.

Federal banking regulators continue to focus on whether financial institutions can demonstrate effective cyber risk management, not simply whether they maintain written policies. In 2026, that distinction matters. Boards, executives, auditors, and examiners increasingly expect evidence that cybersecurity controls are working, exceptions are tracked, third-party risks are understood, and response plans can operate under pressure.

For community banks, the challenge is not usually a lack of effort. It is that cybersecurity work often lives across IT, vendor management, compliance, audit, operations, and executive governance. When those activities are not connected, the institution may have strong individual controls but weak evidence of overall cyber resilience.

Why FFIEC cybersecurity expectations matter now

The FFIEC Cybersecurity Assessment Tool has been retired, but the underlying supervisory themes have not disappeared. Institutions are still expected to understand their inherent risk, maintain controls appropriate to that risk, and demonstrate mature governance over cybersecurity, third parties, incident response, and business continuity.

The practical question for leadership is simple: if an examiner, auditor, insurance carrier, or board member asked for proof today, could the institution show how cyber risk is managed across the business? That proof should not depend on a last-minute scramble. It should come from normal operating routines: risk assessments, board reporting, vulnerability management, access reviews, vendor oversight, tabletop exercises, incident logs, exception tracking, and documented follow-up.

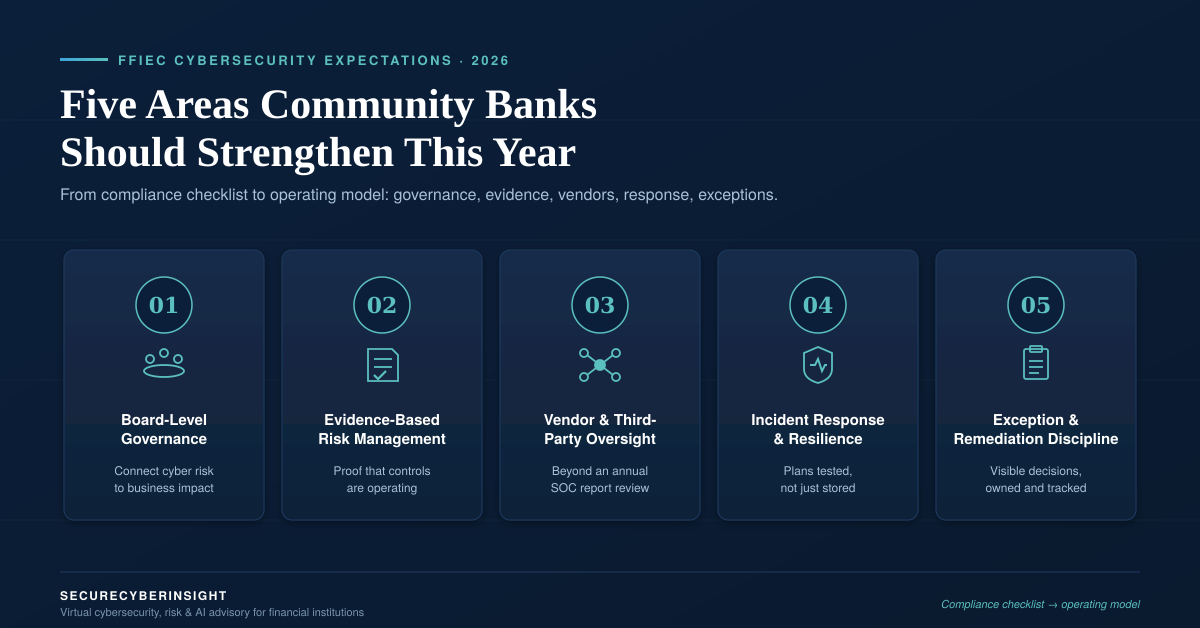

Five areas community banks should strengthen

1. Board-level cybersecurity governance

Cybersecurity is a business risk, not only a technical function. Board reporting should connect cyber risk to operational resilience, customer trust, regulatory expectations, and business impact. Good reporting does not bury directors in tool output. It gives them clear trends, open risks, major exceptions, incident readiness status, and decisions that require executive attention.

A useful board cyber report should answer:

- What changed in our risk profile?

- Which material cyber risks remain open?

- Are key controls operating as expected?

- What third-party or technology dependencies could disrupt service?

- What decisions or investments are needed?

2. Evidence-based cyber risk management

Policies are necessary, but they are not enough. Financial institutions need evidence that controls are operating. That means retaining proof of reviews, approvals, remediation, testing, and escalation.

Examples include completed access reviews, vulnerability remediation records, phishing test results, incident response exercise notes, backup restoration test results, vendor review files, and documented exception approvals. The goal is to make cybersecurity reviewable before an audit or examination begins.

3. Vendor and third-party cyber risk oversight

Banks rely on core processors, cloud providers, managed service providers, fintech partners, payment platforms, and specialized software vendors. FFIEC-aligned cyber risk management requires more than collecting a SOC report once a year.

Institutions should identify critical vendors, understand data access and service dependencies, review security commitments, track open findings, and document risk acceptance decisions. For higher-risk vendors, management should also understand incident notification terms, subcontractor exposure, recovery capabilities, and concentration risk.

4. Incident response and operational resilience

Incident response plans should be tested, not just stored. A strong plan defines roles, escalation paths, communication steps, legal and regulatory considerations, customer impact review, evidence preservation, and recovery priorities.

Tabletop exercises are especially valuable when they force business, technology, compliance, legal, and communications teams to work through realistic scenarios. The most useful outcome is not a perfect exercise. It is a clear list of gaps, owners, and due dates.

5. Exception and remediation discipline

Every institution has exceptions: delayed patches, compensating controls, vendor limitations, legacy systems, deferred projects, or temporary access decisions. The risk is not that exceptions exist. The risk is that they remain undocumented, unowned, or open indefinitely.

A mature program tracks exceptions with business justification, risk rating, compensating controls, owner, approval date, expiration date, and review cadence. This turns exceptions from informal workarounds into visible risk decisions.

A practical 30-day action plan

Community banks do not need to boil the ocean. A focused 30-day review can create momentum:

- Inventory current cybersecurity governance artifacts, including board reports, policies, risk assessments, and open issue logs.

- Identify the top ten pieces of evidence most likely to be requested during an audit, exam, insurance review, or board discussion.

- Review critical vendors and confirm that risk ratings, contracts, SOC reports, and open findings are current.

- Validate incident response contact lists, escalation steps, and tabletop exercise follow-up items.

- Create or refresh a cybersecurity evidence index so documentation is easy to find when needed.

The leadership takeaway

FFIEC cybersecurity expectations are best handled as an operating model, not an annual compliance event. Institutions that maintain clear governance, organized evidence, disciplined vendor oversight, tested response plans, and visible exceptions are better prepared for both regulatory review and real-world disruption.

Cybersecurity maturity does not require unnecessary complexity. It requires repeatable habits, accountable owners, and evidence that the program works when it matters.

Contact SecureCyberInsight to discuss FFIEC readiness for your institution